HARDI Ascend Recap – Phoenix, AZ

HVAC wholesale distributors and the wider HVAC community of HARDI members gathered in early December to discuss the current landscape and future outlook for the industry.

HARDI welcomed more than 1,900 attendees to its 2023 Annual Conference, Ascend, in Phoenix Arizona, including 180 distributors and almost 350 other members (CMG is also a proud member of HARDI). This year’s conference boasted a record number of attendees to date, reaffirming the continued momentum and enthusiasm in the HVAC industry.

Over the course of four days, the HARDI program focused on a wide array of topics ranging from big picture global supply chains and economic outlooks, to more specific topics such as technology, the evolving regulatory environment, working effectively with the contractor / service base, and region- specific economic forecasts for 2024.

CMG’s Key Takeaways from HARDI Ascend

2023 Recap: A Year of Moderation for Distributors

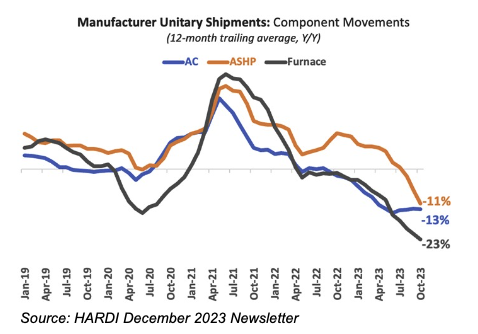

- Following unprecedented profit opportunities largely resulting from OEM price increases in 2021-2022, distributors experienced a year of moderation in 2023, with margins having returned to levels more in-line with historical norms.

- Sales for most distributors, though still positive year-over-year, moderated from the double-digit highs of the previous years. Pricing and inflation remain pivotal for revenue growth, compensating for a nearly 10% decrease in unit shipments.

- According to a conference poll of distributors, approximately 65% reported FY23 financial results that were trending below their early year forecasts, signaling a shift from FY22 peaks.

2024 Outlook: The Word of the Day is “Normalization”

While supply chains continue working toward a return to pre-COVID levels of efficiency, distributors feel a bit more comfortable moderating from a “just-in-case” inventory strategy of stockpiling products that caused peak levels of inventory in 2022 and returning to ‘normalized’ levels of working capital. On the manufacturer front, backlogs are lowering as production picks up and new orders are showing signs of strength. Overall, the industry is moving back to “normalization,” with moderate growth expected, while margins and profitability continuing to move back toward historical (pre-2021) levels.

HVAC Services: Mixed Outlook for 2024 in Contractor End Markets

In the residential sector, housing affordability concerns persist, leading to cautious consumer behavior. Residential new construction markets are expected to remain flat to slightly up through 2024. Conversely, the commercial contractor space shows positivity, with both growing demand and significant backlogs. Factors driving commercial strength are continued investments in manufacturing facilities and robust demand in the retail sector, although office space remains a laggard. While residential HVAC services have been the focal point for M&A consolidation in recent years, we view commercial service markets as an area of potential increased M&A activity, given the attractive growth profiles for investors.

M&A Outlook

A key highlight for CMG at Ascend was an M&A panel consisting of multi-generational family business owners and distributor executives, many with recent merger-and-acquisition experience, who provided several insights into the current M&A landscape.

- Find the Right Partner: Panelists emphasized the importance of aligning with a buyer or investor who share a similar vision and values as the company. Owners should focus beyond the highest dollar amount in a transaction and rather prioritize a partner that values the company’s legacy and is enthusiastic to support its future growth.

- Engage Trusted Advisors: Acknowledging the increasing complexity of M&A deals, owners were advised to enlist trusted advisors. Advisors can play a crucial role in positioning the company effectively, navigating a process involving multiple buyers, and managing due diligence, which in turn allows owners and their teams to concentrate on delivering strong operating results—a key aspect in safeguarding value during an M&A process.

- 2024 Outlook: There was consensus among panelists that 2024 will be a favorable year for M&A in the HVAC distribution sector. The combination of strong balance sheets of corporate (strategic) buyers, normalizing economic and operating conditions, moderating interest rates, and growing confidence in the near-term business outlook for the overall sector creates a healthy environment for M&A in the current market.

Up Next: AHR Expo 2024 Is Around the Corner

CMG is excited to once again attend the AHR Expo, which is quickly approaching in late January. The 2024 AHR Expo kicks off on January 22 in Chicago and is poised to again be the key event for HVAC manufacturing, showcasing the latest advancements in air conditioning, heating, and refrigeration technologies. Last year’s event boasted a diverse array of over 1,900 exhibitors and 60,000 industry attendees, and we expect an even stronger showing this year. Here’s a short preview into a few key themes that are top of mind as we navigate this year’s Expo and meet with industry leaders and HVAC business owners and entrepreneurs:

M&A Dominates Strategic Agendas for Manufacturers and Investors

Independent manufacturers, particularly those offering unique products and/or catering to diverse customer bases, should be aware that the HVAC manufacturing M&A landscape remains robust. Although private equity activity had been tempered by increased borrowing costs and economic uncertainties in 2023, cash-rich public-market manufacturers exhibit sustained interest in inorganic growth for long-term expansion, emerging as resilient acquirers in recent M&A markets. As expectations for interest rate declines in 2024 loom, numerous PE investors have expressed to us an enthusiasm for a renewed push to acquire and grow independent (family & founder-owned) HVAC manufacturing platforms this year.

Innovative Technologies, Sustainability and Strategic Growth

At the heart of the Expo lies a focus on innovative technologies that promise to reshape the HVAC landscape. From advancements in energy efficiency to smart controls, AHR will showcase solutions that cater to the evolving needs of the industry. Sustainability remains a central theme, with a spotlight on eco- friendly, energy-efficient products, including breakthroughs in green technologies, renewable energy integration, and solutions aimed at reducing environmental impact. Not surprisingly, independent companies offering cutting-edge technology and sustainable solutions will emerge as “top of the wish list” targets for M&A acquirers.

Training and Education

Staying Ahead of Regulatory Shifts: The AHR Expo is not just an exhibition of products; it is also a valuable resource for industry knowledge. We eagerly anticipate educational sessions, workshops, and seminars covering the latest trends, best practices, and regulatory updates in the HVAC sector. In particular, we recognize the pivotal role regulatory changes serve in propelling growth within the HVAC sector, acting as a catalyst for innovation and sustained investment interest as HVAC remains a sector of high M&A interest and activity.

Let’s Connect in Chicago

We’re enthusiastic to meet with business owners of innovative companies operating in the HVAC industry and are happy to share insights on how our experience advising founder and multi-generational family businesses can assist you in achieving your business’s strategic initiatives. If you are a business owner attending this year’s AHR Expo and would like to schedule a meeting, please don’t hesitate to reach out to our team, and we will set up time to connect at the Expo.

Q3 2023 M&A Summary

For the overall M&A markets, the third quarter of 2023 signaled a potential rebound in mid-market private- equity-backed M&A, with average purchase price multiples bouncing back nearly a full turn from Q2 2023 levels, aligning with early year figures. Valuations on completed deals averaged 7.5x Trailing Twelve Months (TTM) adjusted EBITDA, a 0.9x increase from Q2.

Despite the uptick in average purchase prices, deal volume remains low, relative to the 2021-2022 timeframe, with 2023 estimated to have closed ~270 transactions. While indicative of a still-disjointed market, the increased purchase prices suggest that strong companies can still attract investment in a high- interest rate environment.

HVAC Sector M&A

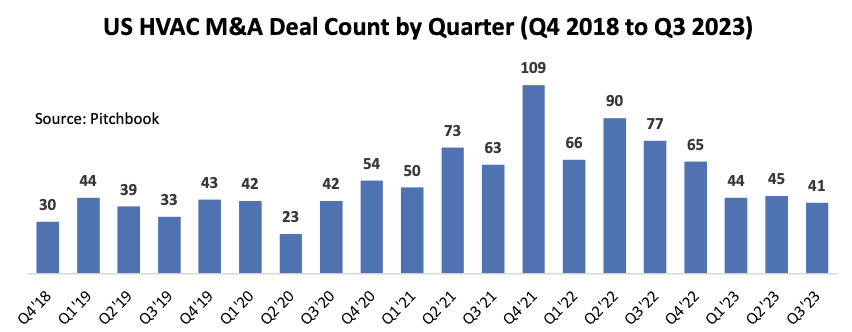

The M&A landscape within the HVAC sector closely mirrored the broader market trends, sustaining a pattern of modest deal volumes when compared to recent years. Nevertheless, amid this backdrop, strategic buyers and private equity firms remain optimistic, buoyed by significant industry tailwinds. Their enthusiasm is evident as they continue to invest in line with the record setting valuations set in the 2021- 2022 period, particularly for emerging platforms. A count of closed deals in the sector (41) is the lowest quarterly figure since Q2 2020, and, on a trailing twelve-month basis, signaled a deal volume decline of 43%.

Despite the downturn in deal volume, Q3 2023 witnessed a surge in average M&A purchase prices across most transaction size tiers, underscoring a critical trend in the market. Notably, transactions exceeding $50 million saw increased average purchase prices, emphasizing the heightened demand for well-prepared, “A- rated” companies. This demand surge appears to stem from a scarcity of supply in the market, making companies with meticulous preparation stand out as coveted assets. Conversely, companies categorized as “B-rated and below” faced delays in entering the market, as they chose to address structural deficiencies before seeking to approach potential acquirers.

Preparation is Key

The above trend concerning “A-rated” companies underscores a compelling narrative – preparation is not just advantageous; it is the defining factor that positions companies as sought-after entities in an M&A market that demands meticulously-positioned opportunities. In an environment where the most well- prepared companies command the highest degree of acquirer attention, this reinforces the importance for businesses to be thoroughly prepared for an M&A process, ensuring they not only attract but also maximize their value to potential buyers.

Contact Us

Whether you are actively considering an exit or just curious about options for the future, we would love to connect, learn more and truly understand your objectives. We are happy to share our insights and help explore strategies to maximize the value of your company and enhance the legacy of your business.

Ramsey Goodrich

203-349-8375 (Direct)

203-554-2435 (Mobile)

RGoodrich@CarterMorse.com

Christopher Reenock

203-349-8376 (Direct)

917-334-1739 (Mobile)

CReenock@CarterMorse.com

Geoff Bradley

203-312-4587 (Mobile)

gbradley@CarterMorse.com